{kind=link}

The discharge of the Federal Reserve’s undefined (SCF) affords a possibility to reassess Individuals’ retirement preparedness as measured by the Nationwide Retirement Danger Index (NRRI).

The NRRI estimates the share of American households which can be vulnerable to being unable to take care of their preretirement lifestyle in retirement.

Setting up the NRRI entails three steps:

1) projecting a alternative price — retirement earnings as a share of preretirement earnings — for a nationally consultant pattern of working-age households;

2) developing a goal alternative price in keeping with sustaining a preretirement lifestyle in retirement;

3) evaluating the projected and goal alternative charges to seek out the share of households “in danger.”

For the reason that final SCF was performed in 2019, the nation skilled a world pandemic and financial disruption, and 2022 was a really unhealthy 12 months for inventory and bond returns. These components would have diminished households’ retirement preparedness. On the similar time, the federal government offered unprecedented fiscal help, employment remained sturdy, dwelling values rose considerably, and the inventory market — even with the drop in 2022 — ended up considerably greater than in 2019.

The 2022 NRRI exhibits that the features in asset values greater than offset the financial disruption to supply the bottom degree of households in danger because the NRRI first began. Particularly, between 2019 and 2022, the share in danger dropped from 47% to 39% (see Determine 1).

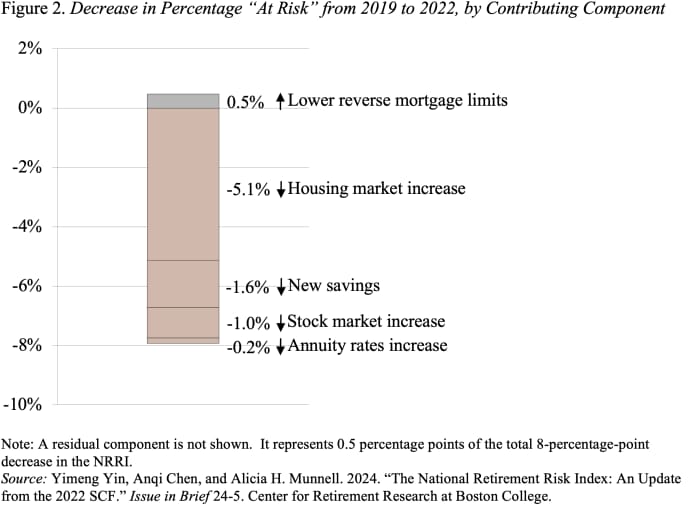

Determine two breaks down the explanations for the large discount within the NRRI. The rise in dwelling costs leads the listing, adopted by new financial savings in the course of the pandemic, and inventory market features. Rising rates of interest had small offsetting results by decreasing how a lot dwelling fairness that households can faucet by means of reverse mortgages.

What do the 2022 outcomes indicate for the longer term? Two main contributors to the beautiful enchancment within the NRRI appear unlikely to persist.

First, housing costs are about 14% above their long-run development for the final 30 years, and should properly revert to development over time.

Second, “new saving” is nearly definitely a one-shot COVID phenomenon. Certainly, private saving charges have returned to prepandemic ranges and so has bank card borrowing. Thus, the spectacular decline within the share of households in danger might not maintain for the longer term.

However assume the excellent news is everlasting, and future NRRIs hover round 40%. That discovering means about two-fifths of at present’s working-age households won’t have sufficient retirement earnings to take care of their preretirement lifestyle. This evaluation continues to verify that we have to repair our retirement system in order that Social Safety is financially sound and employer plan protection is common.